Executive Summary

The question “Who owns ChatGPT?” appears simple. It is not. Ask it in a room of investors, engineers, journalists, and lawyers, and you will get four different-and individually incomplete-answers. Each is right about something and wrong about the whole.

This white paper argues that ownership of a modern AI company like OpenAI cannot be captured by a single name, a single percentage, or a single org-chart box. Instead, it must be understood across four distinct dimensions: the entity that operates the product, the legal entities that sit behind it, the parties that hold economic equity, and the body that exercises governance control. Conflating these dimensions produces the most common errors in public discourse-“Microsoft owns ChatGPT,” “Sam Altman owns OpenAI,” or the belief that the nonprofit’s 26% stake gives it majority control.

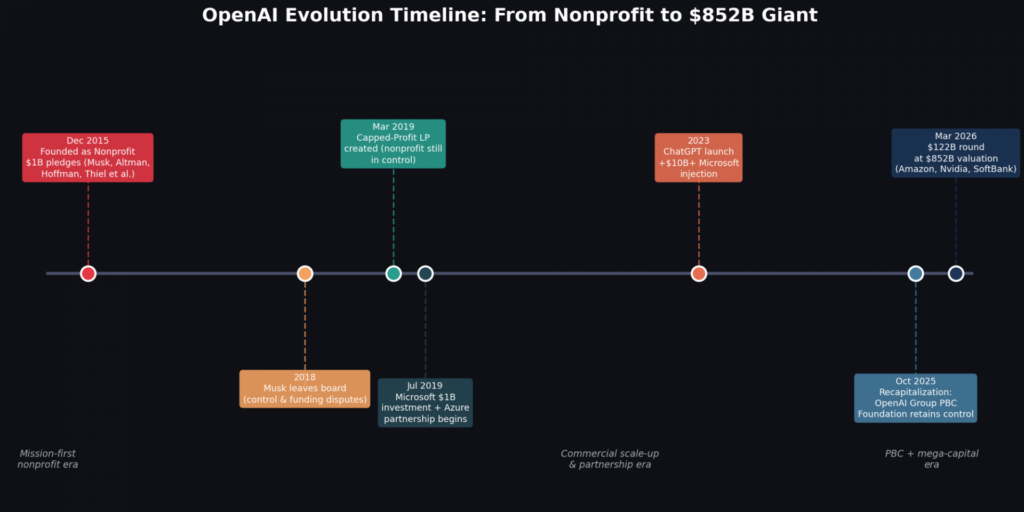

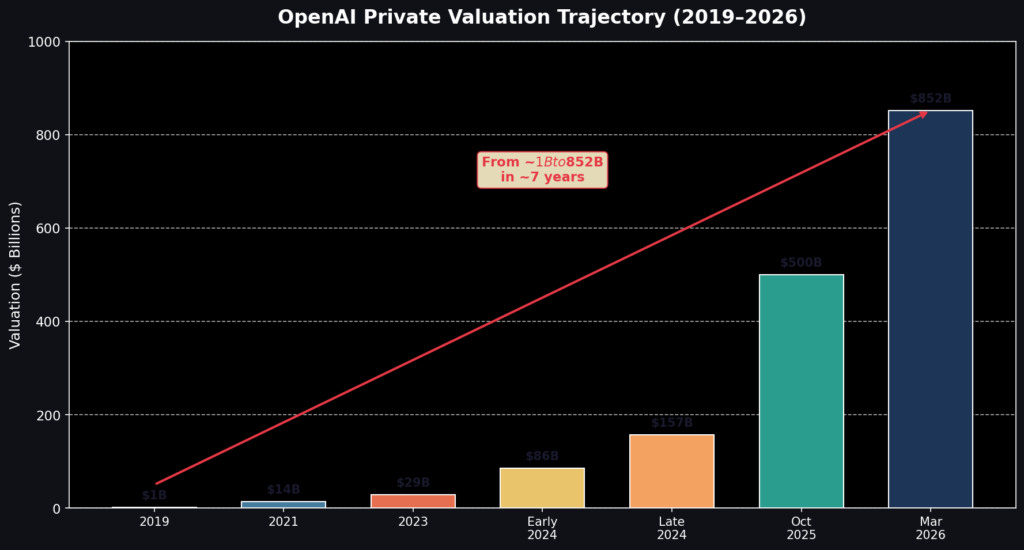

The stakes of getting this right have risen sharply. In October 2025, OpenAI formalized a structure in which a nonprofit foundation controls a for-profit public-benefit corporation. In March 2026, a $122 billion committed-capital round at an $852 billion valuation diluted every prior stakeholder and introduced new hyperscaler anchors-Amazon, Nvidia, and SoftBank. In June 2026, OpenAI confidentially filed for a potential trillion-dollar IPO. Each event reshaped the economic picture while leaving the governance backbone deliberately intact.

Our central finding is a principle we call the equity-governance separation: equity determines economic participation; governance rights determine corporate control. These are legally distinct, and OpenAI’s structure was engineered precisely to keep them apart. A second finding is that the durable answer to “who owns ChatGPT” lies in structure, not percentages-because percentages go stale within quarters, while the Foundation-to-operating-company control chain has survived every restructuring attempt to date.

For executives, communicators, and analysts, the actionable takeaway is a discipline: separate the four ownership dimensions, timestamp every equity figure, and distinguish stable structural facts from volatile financial snapshots. This paper provides the framework to do so.

Introduction

The Landscape

ChatGPT has become one of the most consequential consumer products in technology history, and OpenAI one of the most scrutinized private companies in the world. Yet the ownership of both remains widely misunderstood-not because the facts are hidden, but because the structure is genuinely unusual.

OpenAI does not fit the mental model most people carry for a company. It is neither a straightforward startup with founder equity, nor a public corporation answerable to shareholders, nor a pure nonprofit. It is a hybrid: a nonprofit foundation that controls a for-profit public-benefit corporation, which in turn operates through regional entities that contract with users. Investors-including some of the largest technology companies on earth-hold economic stakes without holding control.

This structure has been in continuous, high-profile flux. Between October 2025 and June 2026 alone, OpenAI reorganized its corporate identity, raised over a hundred billion dollars, and prepared for a public offering that could value it above a trillion dollars. Each of these events changed the answer to “who owns ChatGPT”-but changed it along different dimensions.

The Problem

The core problem is conceptual, not informational. Most answers to “Who owns ChatGPT?” collapse four legally separate questions into one:

- Who provides the service to users?

- Which company operates the commercial business?

- Who holds economic stakes in that company?

- Who controls its board and mission?

When these dimensions blur together, predictable errors follow. Microsoft’s large investment gets mistaken for ownership. The Foundation’s control gets mistaken for majority equity. A confidential IPO filing gets mistaken for a completed public listing. A founder’s historical role gets mistaken for present authority.

These are not pedantic distinctions. They determine who can actually make decisions about the technology, who profits from it, and what protections-if any-future public shareholders will hold.

Why Now

Three developments make this an urgent conversation for 2026.

First, the economic picture is moving faster than public disclosure. The clean ownership split disclosed in October 2025 was diluted within five months by the March 2026 financing, yet no refreshed cap table has been published. Anyone quoting the old figures as current is quoting stale data.

Second, ownership is about to go public. A confidential S-1 signals that public retail and institutional investors may soon join the economic ownership base-raising an unprecedented question about what “ownership” means in a company legally bound to prioritize mission over shareholder returns.

Third, the myths are hardening. As the story gets more complex, simplified narratives (“Microsoft owns it,” “an AGI declaration will blow up the deal”) spread faster than corrections. Some of these narratives were true at one point and are now demonstrably stale. Getting the framework right is the only defense against publishing yesterday’s facts.

The Four Dimensions of Ownership

To answer the question accurately, we must first disaggregate it. Ownership of ChatGPT operates across four dimensions, each governed by a different entity.

Dimension 1: The Operator (Who Provides the Service)

For individual users, the service is provided under contract by OpenAI OpCo, LLC in the United States and most non-EEA regions; other regional OpenAI entities apply elsewhere. This regional qualifier matters. A blanket claim that “users contract with OpenAI OpCo, LLC” is inaccurate for a substantial portion of the global user base, and precision here is what separates a credible reference from a careless one.

Dimension 2: The Legal Entities (What Sits Behind the Product)

OpenAI’s commercial business operates through OpenAI Group PBC, a public-benefit corporation. A public-benefit corporation is legally required to balance its stated mission and broader stakeholder interests against pure profit maximization-a distinction that becomes critical when we consider a future IPO.

Importantly, one should avoid the blanket assertion that OpenAI Group PBC “legally owns every part of ChatGPT.” The precise allocation of ChatGPT-related intellectual property among OpenAI affiliates is not fully public. Being the commercial operator is not the same as being the sole holder of every asset.

Dimension 3: Economic Stakeholders (Who Holds Equity)

This is the dimension most people mean when they ask about ownership-and the one most prone to error, because the numbers change with every financing round.

Key Insight:

The last publicly disclosed cap table dates from October 28, 2025. Any percentage cited without that timestamp is presented as more current than the facts support.

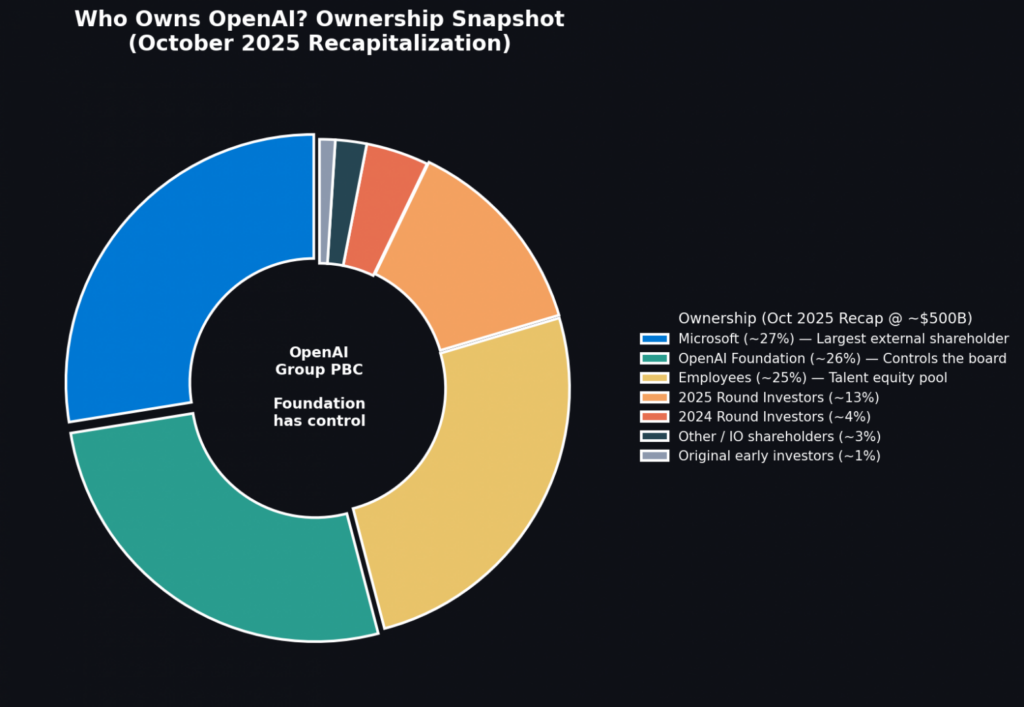

At the October 2025 recapitalization, valued at approximately $500 billion, OpenAI disclosed an ownership baseline across three groups.

The following chart shows that disclosed baseline-which should always be labeled as a pre-dilution snapshot.

OpenAI Economic Ownership Snapshot (Oct 28, 2025)

| Ownership (%) | |

| Microsoft | 27 |

| OpenAI Foundation | 26 |

| Employees and other investors | 47 |

Estimated economic ownership of OpenAI as of October 28, 2025, split between Microsoft, OpenAI Foundation, and employees/other investors

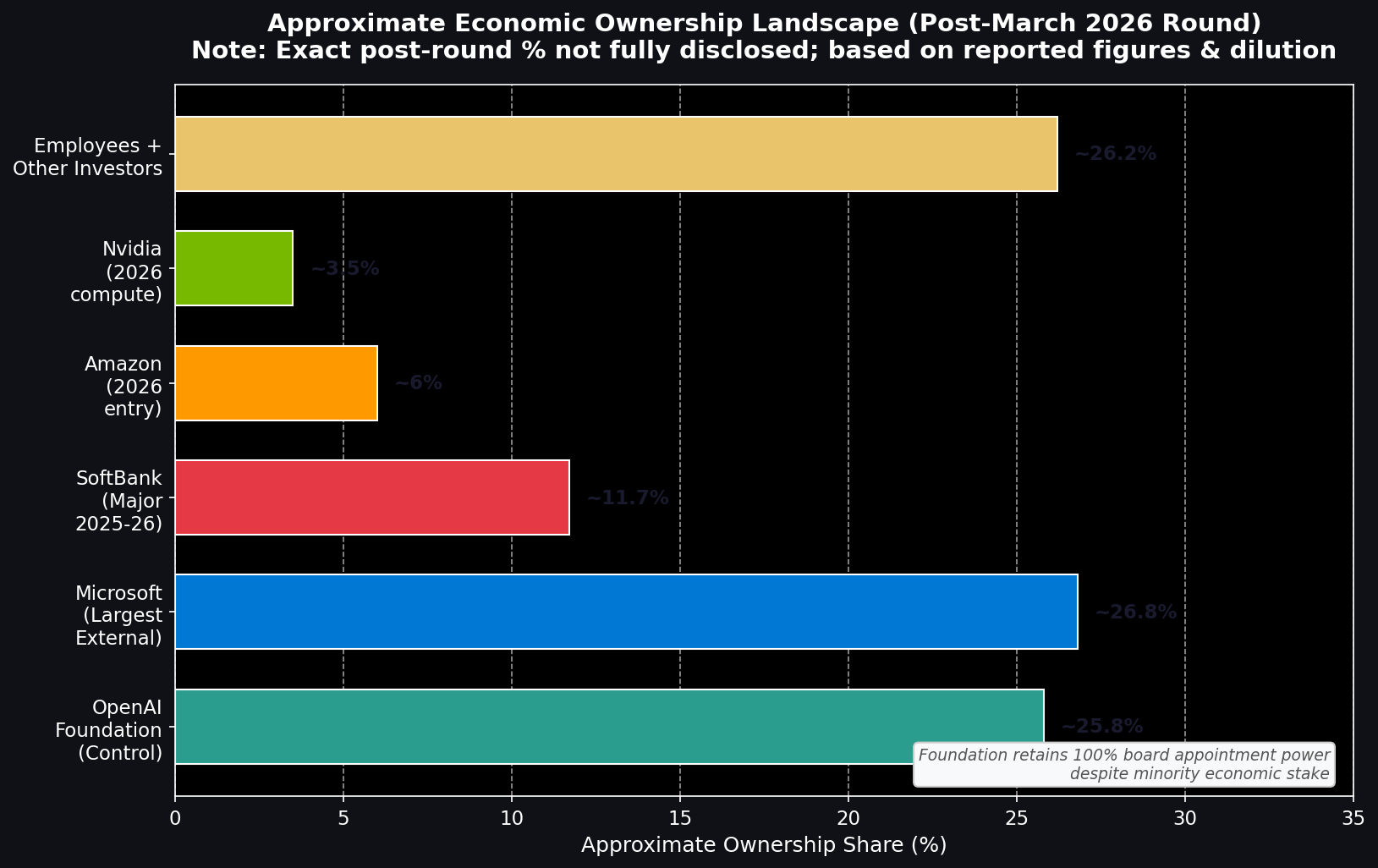

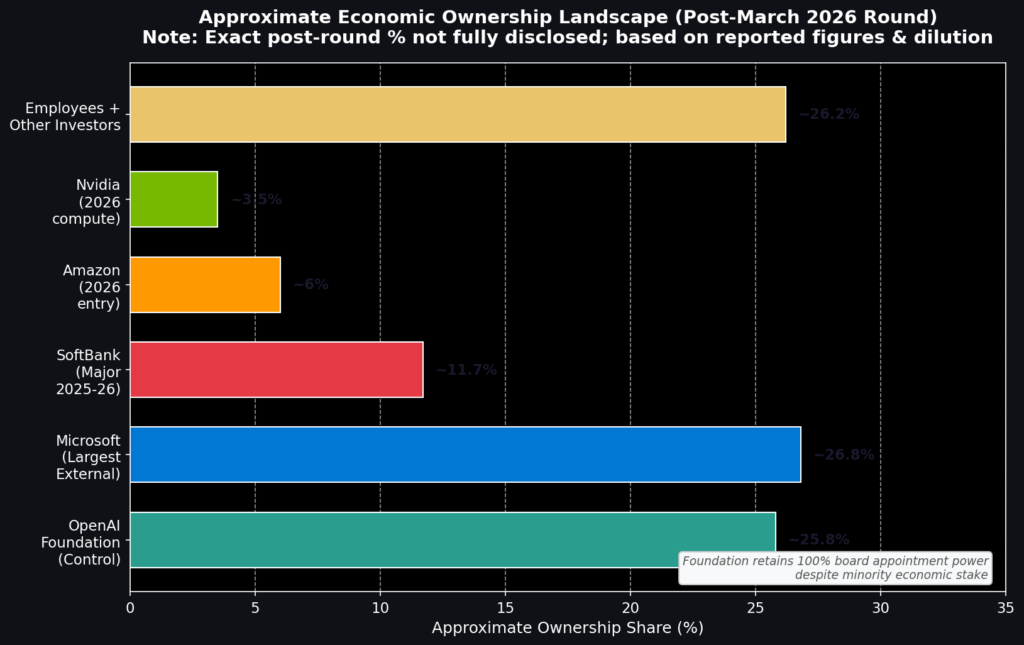

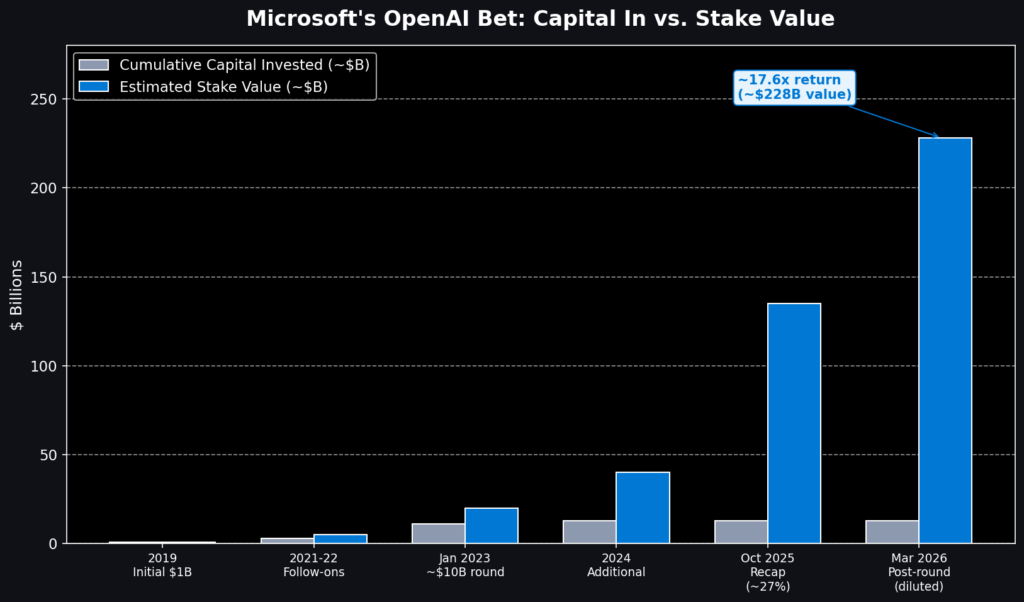

These figures-Microsoft approximately 27%, the OpenAI Foundation approximately 26%, and employees and other investors approximately 47%-represent a historical baseline, not a current reality. The March 31, 2026 financing closed at $122 billion in committed capital at an $852 billion post-money valuation, anchored by Amazon (a reported $50 billion commitment, with a large portion contingent on an IPO or an AGI milestone), Nvidia, and SoftBank (approximately $30 billion each). This round diluted every prior stakeholder and transformed the cap table from a concentrated two-player dynamic (Microsoft versus the Foundation) into a distributed structure with five major economic anchors.

No complete post-March-2026 cap table has been publicly released. The exact current percentages are, at the time of this writing, genuinely unknown.

Dimension 4: Governance Control (Who Controls the Board and Mission)

Ultimate control rests with the OpenAI Foundation, the nonprofit. Its authority is structural, not economic: it appoints and can replace the board of OpenAI Group PBC regardless of how much equity any investor holds. Critically, this control does not derive from its 26% stake. A minority equity holder controls the entire enterprise through governance rights alone.

This control survived a near-death experience. Discussions in 2024–2025 explored restructuring in ways that would have altered nonprofit control; after significant external scrutiny, including from state attorneys general, OpenAI reaffirmed on May 5, 2025 that the nonprofit would continue to control the commercial organization. The governance backbone held.

The Equity-Governance Separation Framework

The single most important concept in this entire analysis can be stated in one line:

Key Insight:

Equity determines economic participation; governance rights determine corporate control. These are legally distinct, and OpenAI’s structure was engineered to keep them apart.

This principle explains why nearly every popular misconception about ChatGPT ownership is wrong. Once you internalize that economic stake and control authority are separate axes, the confusion dissolves.

Applying the Framework to Common Claims

The framework acts as a diagnostic tool. Consider how it resolves the four most common ownership claims:

| Claim | Traditional (Conflated) Reasoning | Framework-Corrected Analysis |

|---|---|---|

| “Microsoft owns ChatGPT” | Microsoft invested billions and held the largest outside stake, so it must control the product | Microsoft holds equity, a non-exclusive license, and a cloud partnership-but no governance authority over the board or mission |

| “Sam Altman owns OpenAI” | He is the CEO and public face, so he must be the owner | CEO is an executive role, not an ownership role; no public filing supports a quantifiable personal equity stake |

| “The Foundation’s 26% gives it control” | It controls the company, so it must hold a majority | Control comes from structural board-appointment rights, not from majority equity |

| “An AGI declaration will end Microsoft’s access” | An old clause tied Microsoft’s license to a pre-AGI threshold | The clause was amended; AGI is now a verification event, not a kill-switch (see below) |

The Corrected AGI Module: Verification Event, Not Kill-Switch

One narrative deserves special correction because it is both widely repeated and now demonstrably stale.

The original 2019 arrangement reportedly allowed a unilateral AGI declaration to sever Microsoft’s license to OpenAI’s technology. This “AGI kill-switch” story circulated widely. It is no longer accurate.

Across two amendments-October 28, 2025 and April 27, 2026-the clause was defused. A unilateral declaration became an independent-panel verification. Access termination became access extended through 2032, and Microsoft’s model and product IP rights now explicitly include post-AGI models, subject to appropriate safety guardrails.

The corrected framing:

An AGI declaration is now a verification and contractual milestone-not an automatic termination of Microsoft’s access to OpenAI technology. It may still affect economics and revenue-share timelines, but it does not sever the license.

One caveat must be kept distinct: Amazon’s large contingent tranche (a reported $35 billion) is tied to an IPO or AGI milestone. This is an investor-specific vesting condition, not a licensing kill-switch. Conflating Amazon’s vesting condition with Microsoft’s licensing terms produces a false narrative. They are two different “AGI” facts pointing in opposite directions.

The Practical-Reality Caveat

The framework describes de jure control-control on paper. Honest analysis requires one qualification, offered here as analysis rather than as a competing ownership finding.

Formal governance authority does not eliminate operational dependency. ChatGPT requires enormous ongoing capital and compute from partners like Microsoft and Amazon. In principle, decisions that would severely damage investor economics could face practical constraints-withheld resources, covenants, or partner friction-even without any formal change in governance. This is a real dynamic that sophisticated observers should hold in mind.

But it should not become the headline. The stable, defensible truth is the equity-governance separation and the Foundation’s disclosed control. The practical-reality caveat supplements that structure; it does not overturn it. Notably, the more dramatic “hyperscalers own the engine” narrative aged worse than the cautious structural account: the spicy AGI kill-switch story went stale, while the careful “don’t overstate the constraints” instinct proved correct.

Key Findings

- Ownership is four questions, not one: Operator, legal entity, economic stakeholder, and governance controller are distinct dimensions, and most public errors come from collapsing them.

- Governance is separated from equity by design: The OpenAI Foundation controls the enterprise through board-appointment rights with roughly a quarter of the equity-proving that control and ownership are legally independent.

- Every equity figure is perishable: The October 2025 baseline (approximately Microsoft 27%, Foundation 26%, employees and others 47%) was diluted by the March 2026 round and no longer reflects current reality; no refreshed cap table is public.

- The AGI kill-switch narrative is stale: Amendments in 2025 and 2026 converted an AGI declaration from a license-terminating event into a verification milestone, with Microsoft’s access contractually extended through 2032, including post-AGI models.

- The IPO raises an unresolved structural tension: A public-benefit corporation whose charter subordinates profit to mission would offer public shareholders economic exposure without the standard expectation that the board must maximize returns-a genuinely novel proposition at a near-trillion-dollar scale.

- Structure is durable; percentages are not: Across multiple restructurings and financings, the Foundation-to-PBC-to-operating-entity control chain survived intact-making structure, not equity share, the stable answer to the ownership question.

Recommendations

For Communications and Content Teams

- Timestamp every equity figure. Never present the October 2025 percentages as current. Label them explicitly as “as of October 28, 2025, pre-March-2026 dilution.”

- Carry the regional qualifier. State the full “in the U.S. and most non-EEA regions, OpenAI OpCo, LLC; other regional entities apply elsewhere” on first mention in each major section, then use “the applicable regional operating entity” thereafter to keep prose readable without dropping the legal substance.

- Lead with structure, not numbers. The durable answer is the Foundation → PBC → operating-entity chain. Percentages are the volatile layer; structure is the stable layer.

- Include a visible “last verified” stamp. This lets the content survive a reader arriving months later with a leaked or updated filing.

For Analysts and Investors

- Separate licensing terms from investment terms. Microsoft’s license (extended through 2032) and Amazon’s contingent tranche (tied to IPO or AGI) are different instruments. Do not let one narrative bleed into the other.

- Treat “committed capital” and “cash received” as different. A $122 billion committed-capital round is not $122 billion in the bank; portions may be tranched, conditional, or in the form of compute credits.

- Distinguish structural tension from stated risk. The “IPO paradox”-public equity in a mission-first PBC-is a real structural tension worth analyzing, but it should be framed as such, not as an assertion about the contents of a confidential filing no one has read.

For Operators Tracking the Story

- Monitor the right trigger. A confidential S-1 does not appear on public regulatory databases-that is the entire point of confidential submission. The correct monitoring trigger is the transition event: the first public S-1 or amended filing (the unsealing, typically shortly before a roadshow), plus the company’s own newsroom. Pointing a monitor at a public filing database today for a confidential draft returns nothing.

- Automate the unsealing alert, not a manual search. The single event that would rewrite the entire ownership picture is the S-1 going public. Automate detection of that specific transition rather than relying on periodic manual checks.

Conclusion

We opened with a deceptively simple question: Who owns ChatGPT? The honest answer is that no single name captures the truth, because “ownership” is not one thing.

ChatGPT is an OpenAI product. In the United States and most non-EEA regions, individual users contract with OpenAI OpCo, LLC, with other regional entities applying elsewhere. The commercial business operates through OpenAI Group PBC. Economic stakes are spread across Microsoft, the OpenAI Foundation, employees, and newer anchors including Amazon, Nvidia, and SoftBank-in proportions that shifted with the March 2026 financing and remain undisclosed in their current form. And ultimate control rests with the nonprofit OpenAI Foundation, whose governance authority is deliberately insulated from the economic cap table.

The reader who began this paper hoping for a name now has something more useful: a framework. The equity-governance separation is the master key. It explains why Microsoft’s investment is not control, why the Foundation’s minority stake is nonetheless decisive, why a founder is not automatically an owner, and why a confidential IPO filing changes economics without changing command.

That framework is also what makes any answer durable. Percentages will keep moving-the S-1, when it unseals, will be the first document to answer the economic question with real numbers rather than estimates pieced together from press releases. But the structural answer has proven remarkably stable, surviving governance battles, a massive financing round, and IPO preparation. Whoever comes to own the economic upside of ChatGPT, the architecture is designed so that public shareholders will hold stake, not steering.

The lesson extends beyond OpenAI. As more AI companies adopt hybrid nonprofit-controlled, public-benefit structures, the ability to separate economic ownership from governance control will become a core literacy-for investors, regulators, journalists, and the public alike. The question is no longer “who owns it,” but “who owns which dimension of it.” That is the question worth learning to ask.

Last verified: July 17, 2026. This analysis reflects publicly available information as of the publication date. The single event most likely to materially change this picture is the public unsealing of OpenAI’s S-1 registration statement, which would provide the first refreshed, authoritative ownership disclosure since October 2025.